The R Package diseq:

Estimation Methods for Markets in Equilibrium and Disequilibrium

July 6th, 2021

useR! The R Conference

Pantelis Karapanagiotis

karapanagiotis[at]ebs[dot]edu

@pi_kappa_

EBS University Wiesbaden, Leibniz Institute for Financial Research SAFE

Markets in Equilibrium

- Equilibrium concepts are analytically convenient.

- Equilibrium models constitute reasonable econometric approximations on many occasions.

Markets in Disequilibrium

- On others… not so much

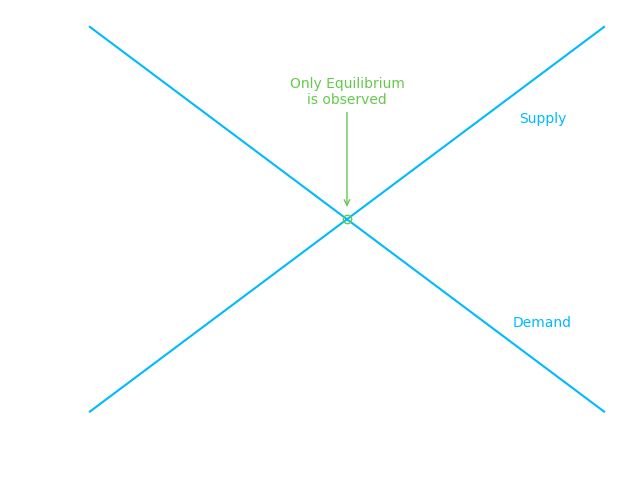

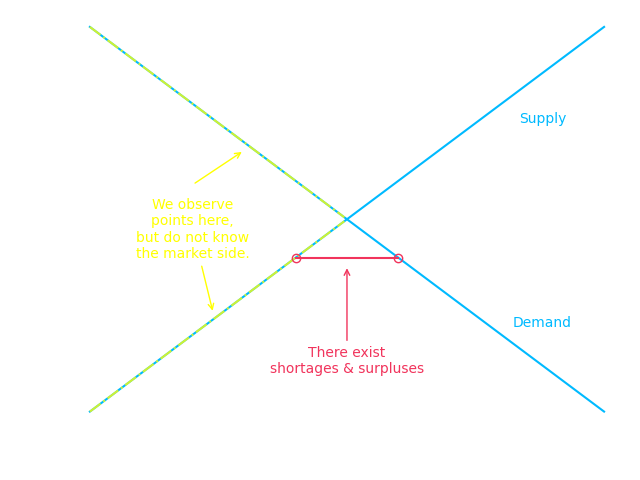

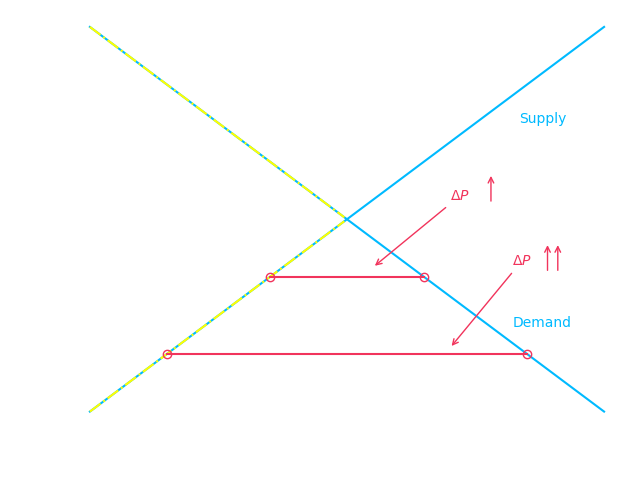

Market Clearing vs Short Side Rule

\begin{align*}

Q_{nt} &= D_{nt} = S_{nt}

\end{align*}

\begin{align*}

Q_{nt} &= \min\{D_{nt},S_{nt}\}

\end{align*}

Design goals

- Simple, approachable, common estimation interface for all market models.

- Fast estimation routines.

- Post estimation analytics.

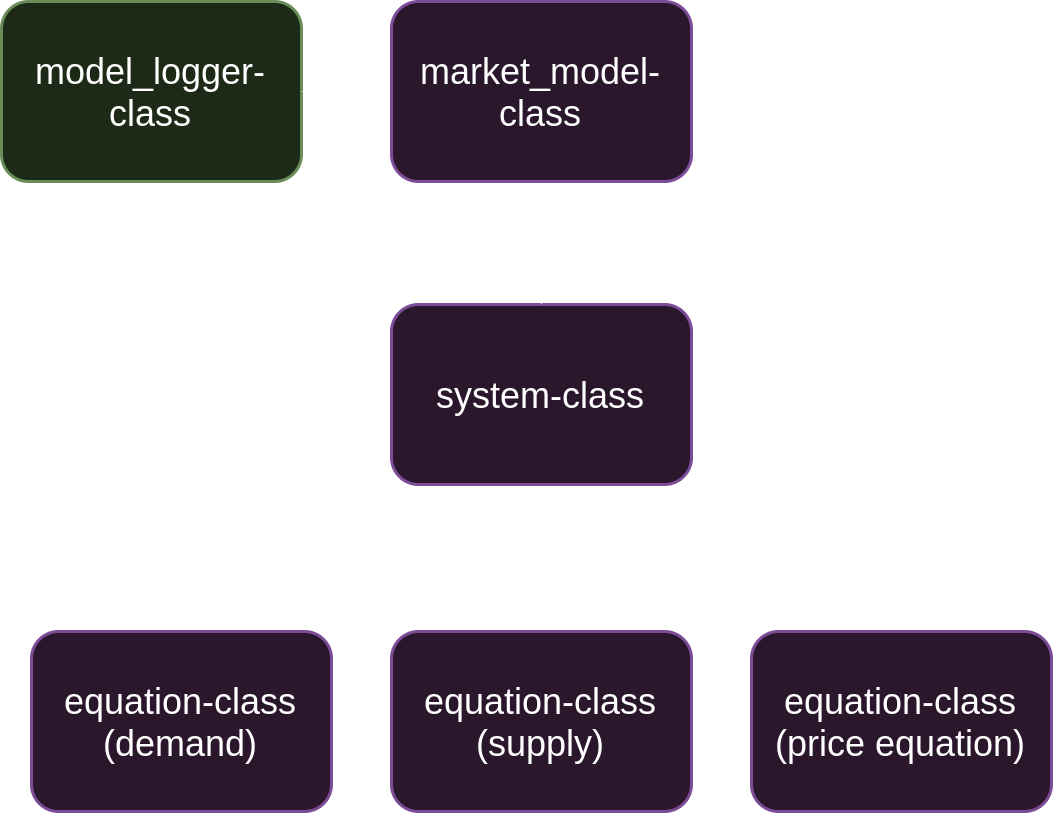

Implementation

- Simple, approachable, common estimation interface for all market models.

- Object oriented design architecture. Polymorphic estimation (and other) calls.

- Fast estimation routines.

- Estimation using analytic gradient expressions by default.

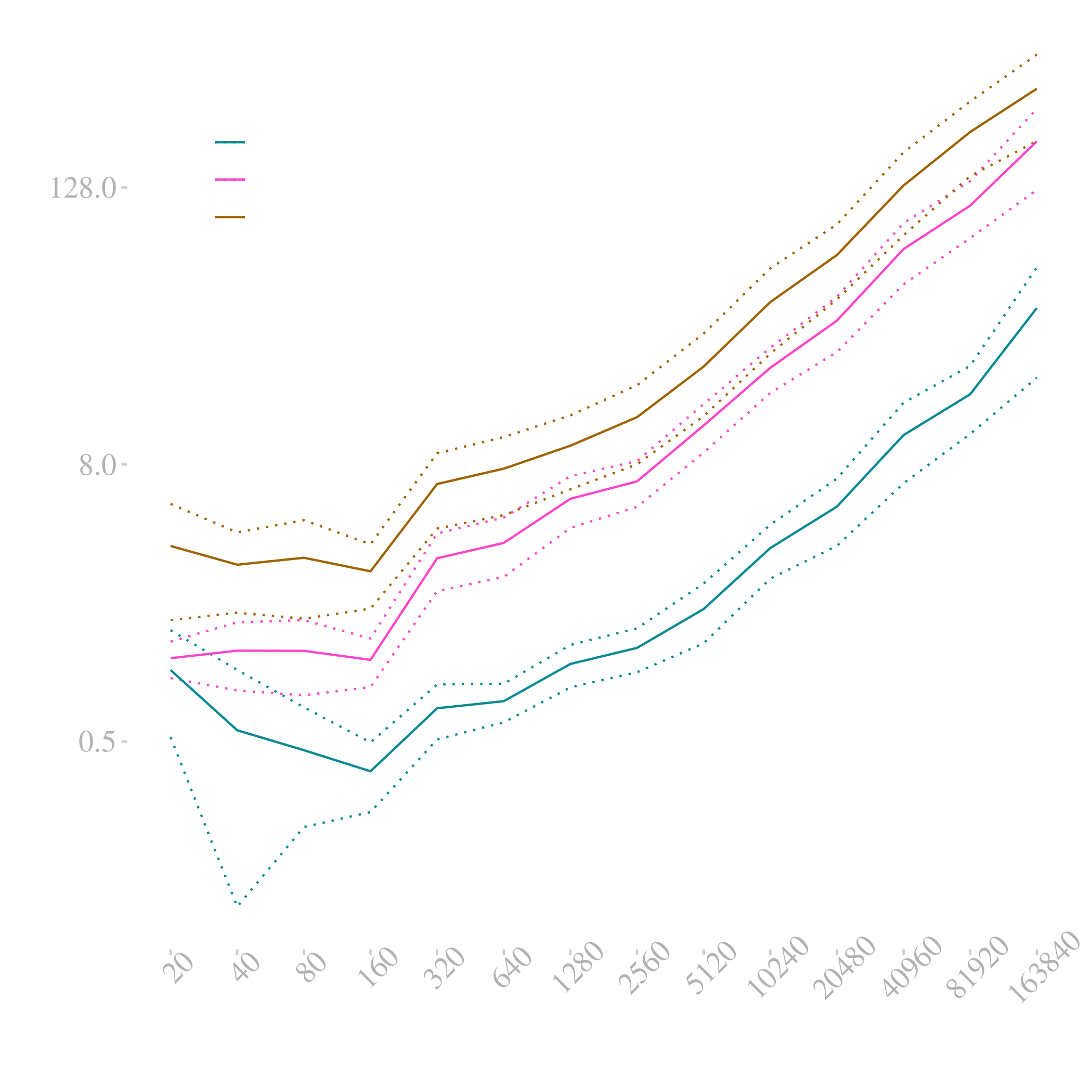

- Performance gains are documented by extensive benchmarking estimations with simulated data.

- Post estimation analytics.

- Predicted demanded and supplied quantities. Aggregation.

- Analysis of shortages.

- Marginal effects.

Architecture overview

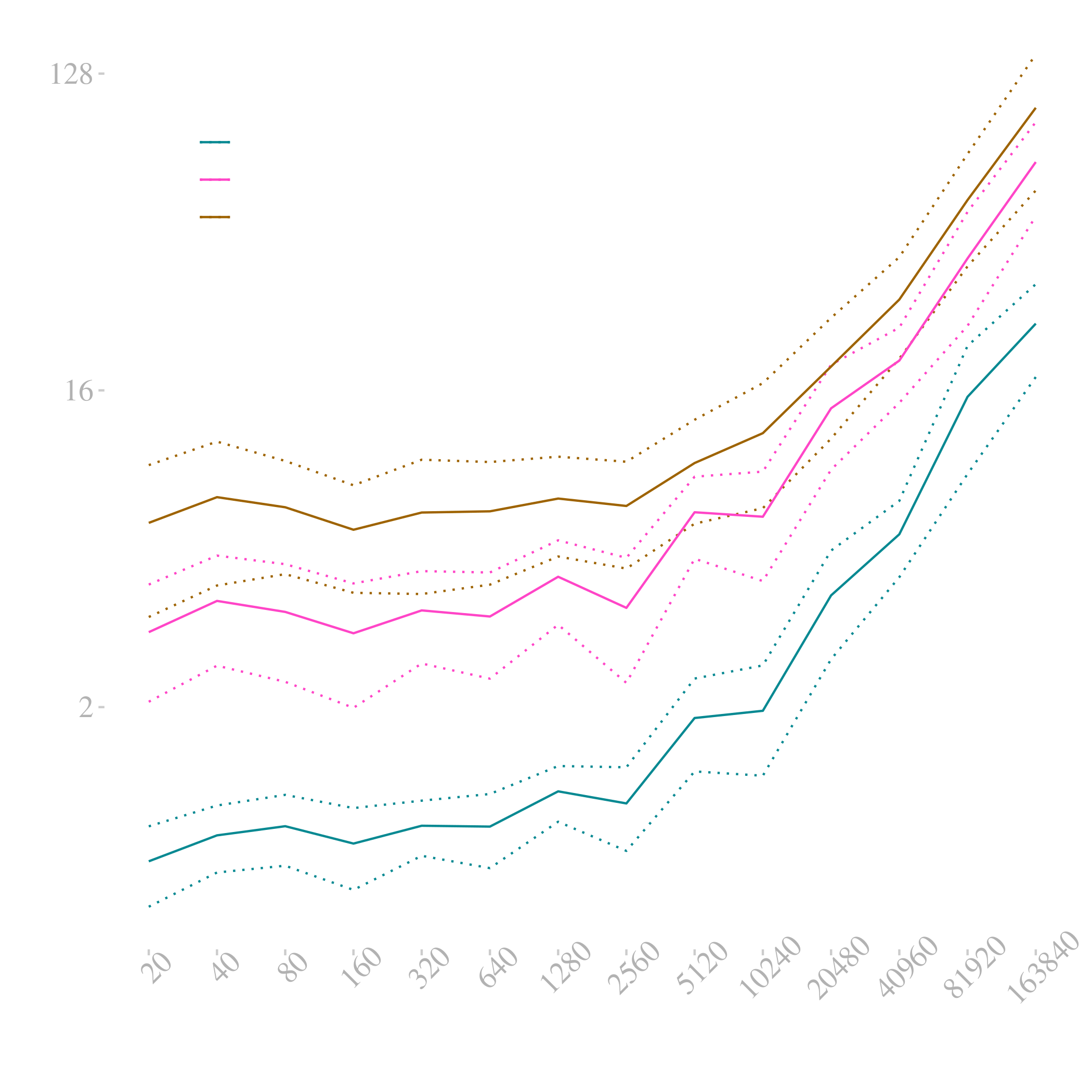

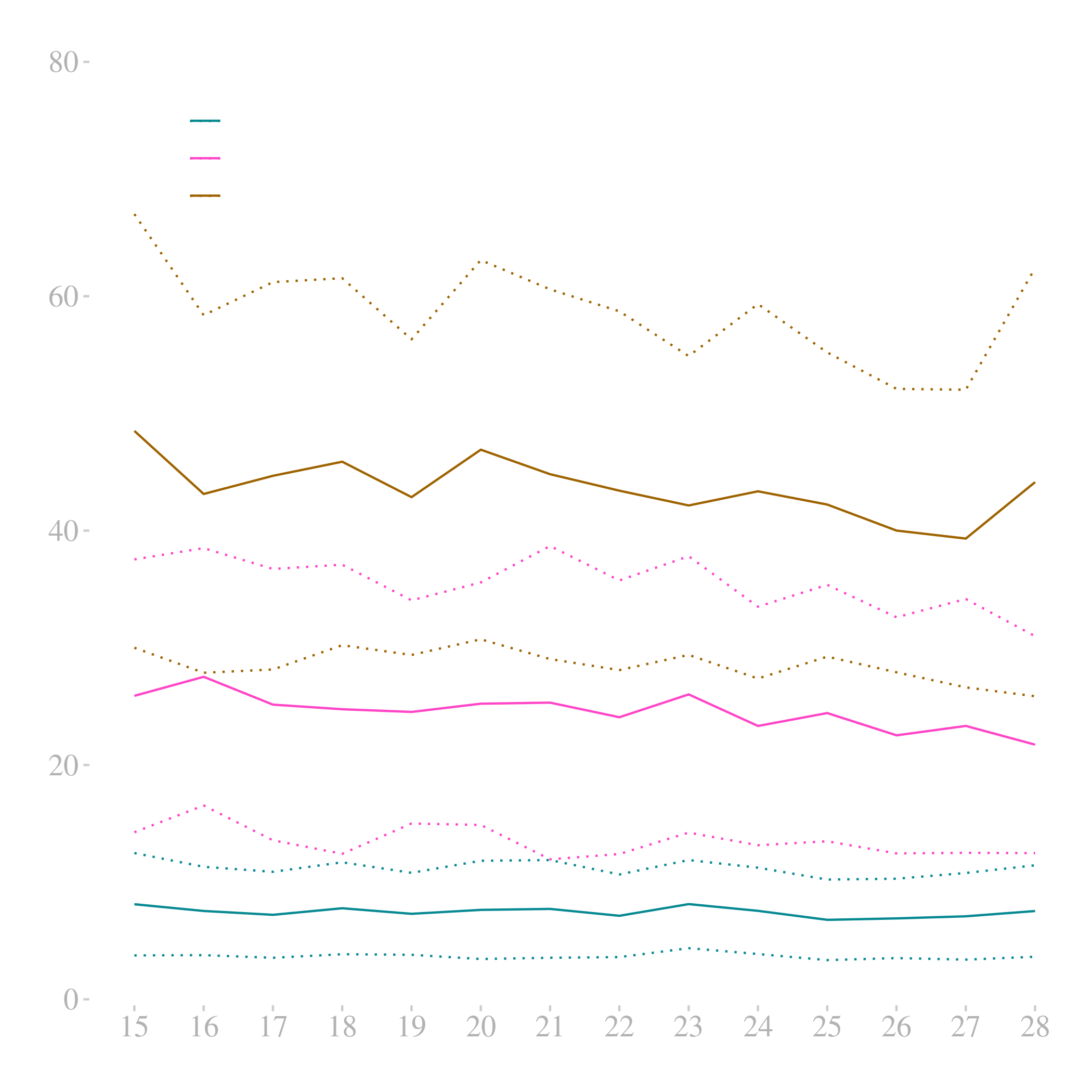

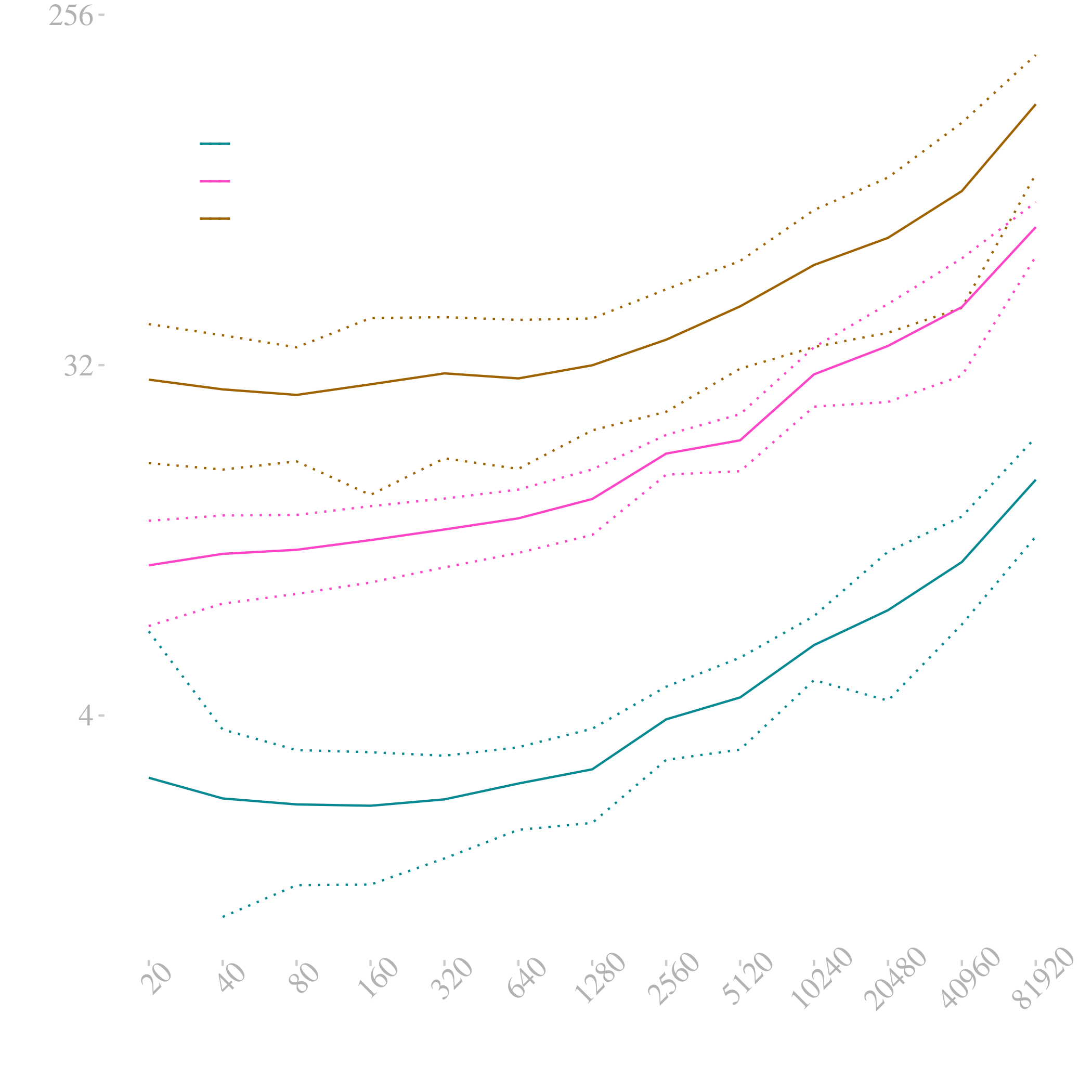

Basic model estimation benchmarks

Model specification

key_columns <- c("ID", "TREND")

quantity_column <- "HS"

price_column <- "RM"

time_column <- "TREND"

demand_specification <- "TREND + W + CSHS + L1RM + L2RM + MONTH"

supply_specification <- "TREND + W + L1RM + MA6DSF + MA3DHF + MONTH"

correlated_shocks <- FALSE

verbose <- 3

Model initialization

equilibrium_mdl <- new(

"equilibrium_model",

key_columns, quantity_column, price_column,

paste(price_column, demand_specification, sep = "+"),

paste(price_column, supply_specification, sep = "+"),

house_data,

correlated_shocks = correlated_shocks, verbose = verbose)

basic_mdl <- new(

"diseq_basic",

key_columns, quantity_column, price_column,

paste(price_column, demand_specification, sep = "+"),

paste(price_column, supply_specification, sep = "+"),

house_data,

correlated_shocks = correlated_shocks, verbose = verbose)

directional_mdl <- new(

"diseq_directional",

key_columns, time_column, quantity_column, price_column,

paste(price_column, demand_specification, sep = "+"),

supply_specification,

house_data,

correlated_shocks = correlated_shocks, verbose = verbose)

deterministic_adjustment_mdl <- new(

"diseq_deterministic_adjustment",

key_columns, time_column, quantity_column, price_column,

paste(price_column, demand_specification, sep = "+"),

paste(price_column, supply_specification, sep = "+"),

house_data,

correlated_shocks = correlated_shocks, verbose = verbose)

Model estimation

optimization_control <- list(maxit = 50000)

equilibrium_est <- estimate(equilibrium_mdl, control = optimization_control)

basic_est <- estimate(basic_mdl, control = optimization_control,

start = equilibrium_est@coef)

directional_est <- estimate(directional_mdl, method = "Nelder-Mead",

control = optimization_control)

deterministic_adjustment_est <- estimate(deterministic_adjustment_mdl,

control = optimization_control)

The R Package diseq:

Estimation Methods for Markets in Equilibrium and Disequilibrium

- Provides estimation solutions with unavailable alternatives.

- Simple market model estimation interface.

- Fast implementation of estimation routines.

- Post estimation analysis tools.

- Where to go from here?

- Additional models: Mayer, Madden, Jin & Tran (2015), Loberto & Zollino (2018).

- Alternative estimation methods: Quandt & Ramsey (1978), Zilinskas & Bogle (2006).

- Disequilibrium tests: Quandt (1978), Hwang (1980).

Pantelis Karapanagiotis

karapanagiotis[at]ebs[dot]edu

References

- [mayer2015] Mayer, Madden, Jin & Tran, Modelling OECD broadband subscriptions in disequilibrium, Technological Forecasting and Social Change, 90(PB), 476-486 (2015). doi.

- [loberto2016] Loberto & Zollino, Housing and Credit Markets in Italy in Times of Crisis, Bank of Italy, (2018).

- [quandt1978estimating] Quandt & Ramsey, Estimating mixtures of normal distributions and switching regressions, Journal of the American Statistical Association, 73(364), 730-738 (1978). doi.

- [zilinskas2006] Zilinskas & Bogle, Balanced random interval arithmetic in market model estimation, European Journal of Operational Research, 175(3), 1367-1378 (2006). doi.

- [quandt1978tests] Quandt, Tests of the Equilibrium vs. Disequilibrium Hypotheses, International Economic Review, 19(2), 435 (1978). doi.

- [hwang1980] Hwang, A test of a disequilibrium model, Journal of Econometrics, 12(3), 319-333 (1980). doi.

- [blpestimator2019] BLPestimatoR, BLP Demand Estimation, By Brunner D., Weiser C. & Romahn A. Distributed by CRAN, (2019).

- [miceconaids2017] MicEconAids, Demand analysis with the almost ideal demand system, By Henningsen A. Distributed by CRAN, (2017).

- [disequilibrium2020] Disequilibrium, Disequilibrium Models, By Latshaw N. & Guggisberg M. Distributed by CRAN, (2020).

- [henningsen2007] Henningsen & Hamann, systemfit : A Package for Estimating Systems of Simultaneous Equations in R, Journal of Statistical Software, 23(4), 1-40 (2007). link. doi.

- [bbmle2020] Bbmle, Tools for General Maximum Likelihood Estimation, By Bolker B, R Development Core Team & Giné-Vázquez I. Distributed by CRAN, (2020).

- [zellner1962] Zellner & Theil, Three-Stage Least Squares: Simultaneous Estimation of Simultaneous Equations, Econometrica, 30(1), 54 (1962). doi.

- [balestra1987] Balestra & Varadharajan-Krishnakumar, Full information estimations of a system of simultaneous equations with error component structure, Econometric Theory, 3(2), 223-246 (1987). doi.

- [fair1972] Fair & Jaffee, Methods of Estimation for Markets in Disequilibrium, Econometrica, 40(3), 497 (1972). doi.

- [amemiya1974] Amemiya, A Note on a Fair and Jaffee Model, Econometrica, 42(4), 759 (1974). doi.

- [maddala1974] Maddala & Nelson, Maximum Likelihood Methods for Models of Markets in Disequilibrium, Econometrica, 42(6), 1013 (1974). doi.

- [maddala1986] Maddala, Disequilibrium, self-selection, and switching models, , 3, in: Handbook of Econometrics (1986).

- [userp] Economic Report of the President, President and Council of Economic Advisers (U.S.), (1947).

- [fair1971] Fair, A short-run forecasting model of the United States economy, Heath Lexington Books (1971).

- [usfrb] Federal Reserve Bulletin, Board of Governors of the Federal Reserve System (U.S.), 1935- and Federal Reserve Board, (1914).

Appendix

Previous research and related software

- Similar and alternative software

- Demand estimation: BLPestimatoR (2019), MicEconAids (2017)

- Disequilibrium estimation: Disequilibrium (2020)

- Powered by

- R packages: Henningsen & Hamann (2007), Bbmle (2020)

- Native libraries: GNU Scientific Library

- Estimation theory:

- Equilibrium: Zellner & Theil (1962), Balestra & Varadharajan-Krishnakumar (1987)

- Disequilibrium: Fair & Jaffee (1972), Amemiya (1974), Maddala & Nelson (1974), Maddala (1986), Quandt & Ramsey (1978).

Market models

The equilibrium model

\begin{align}

\begin{aligned}

D_{nt} &= X_{d,nt}'\beta_{d} + P_{nt}\alpha_{d} + u_{d,nt}, \\

S_{nt} &= X_{s,nt}'\beta_{s} + P_{nt}\alpha_{s} + u_{s,nt}, \\

Q_{nt} &= D_{nt} = S_{nt} .

\end{aligned} \tag{E} \label{eq:model:equilibrium}

\end{align}

- Assumes that market clearing always holds.

- Estimated with 2SLS, 3SLS, and FIML. The last two methods are asymptotically equivalent.

The basic model

\begin{align}

\begin{aligned}

D_{nt} &= X_{d,nt}'\beta_{d} + u_{d,nt}, \\

S_{nt} &= X_{s,nt}'\beta_{s} + u_{s,nt}, \\

Q_{nt} &= \min\{D_{nt},S_{nt}\} .

\end{aligned} \tag{B} \label{eq:model:basic}

\end{align}

- Instead of market clearing, the short side rule governs the market. No price dynamics.

The directional model

\begin{align}

\begin{aligned}

D_{nt} &= X_{d,nt}'\beta_{d} + u_{d,nt}, \\

S_{nt} &= X_{s,nt}'\beta_{s} + u_{s,nt}, \\

Q_{nt} &= \min\{D_{nt},S_{nt}\}, \\

\Delta P_{nt} &\ge 0 \implies D_{nt} \ge S_{nt}.

\end{aligned} \tag{D} \label{eq:model:directional}

\end{align}

- Sample separation based on price changes (One directional assumption however).

The deterministic adjustment model

\begin{align}

\begin{aligned}

D_{nt} &= X_{d,nt}'\beta_{d} + P_{nt}\alpha_{d} + u_{d,nt}, \\

S_{nt} &= X_{s,nt}'\beta_{s} + P_{nt}\alpha_{s} + u_{s,nt}, \\

Q_{nt} &= \min\{D_{nt},S_{nt}\}, \\

\Delta P_{nt} &= \frac{1}{\gamma} \left( D_{nt} - S_{nt} \right).

\end{aligned} \tag{DA} \label{eq:model:deterministic_adjustment}

\end{align}

- Sample separation based on price movements, but this time in a quantitative nature. Price changes are analogous to shortages/surpluses.

The stochastic adjustment model

\begin{align}

\begin{aligned}

D_{nt} &= X_{d,nt}'\beta_{d} + P_{nt}\alpha_{d} + u_{d,nt}, \\

S_{nt} &= X_{s,nt}'\beta_{s} + P_{nt}\alpha_{s} + u_{s,nt}, \\

Q_{nt} &= \min\{D_{nt},S_{nt}\}, \\

\Delta P_{nt} &= \frac{1}{\gamma} \left( D_{nt} - S_{nt} \right) + X_{p,nt}'\beta_{p} + u_{p,nt}.

\end{aligned} \tag{SA} \label{eq:model:stochastic_adjustment}

\end{align}

- No sample separation. Price dynamics are stochastic.

Package design

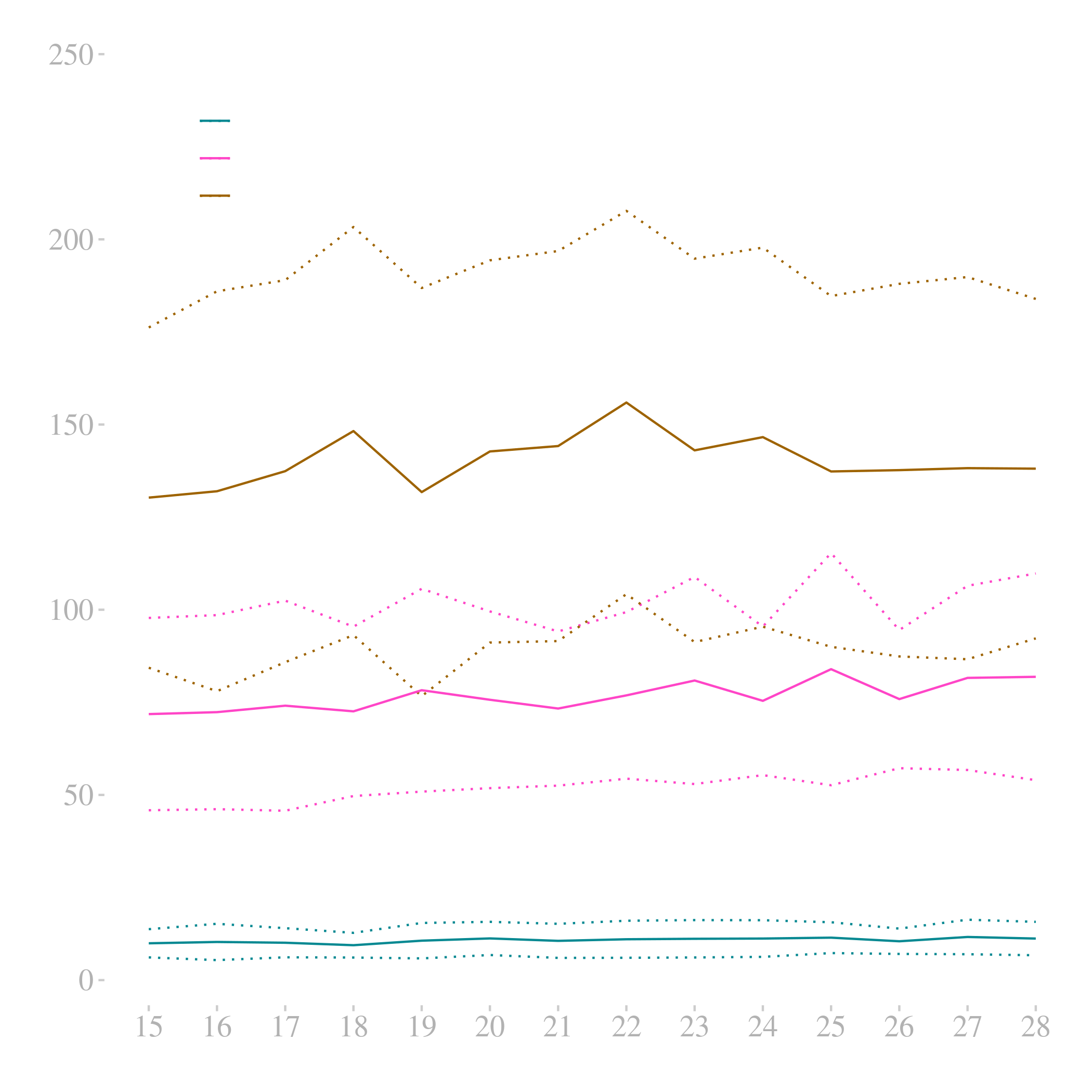

Comparison of equilibrium estimation methods and tools

seed <- 25

parameters <- list(

nobs = 4000, tobs = 5,

alpha_d = -0.7, beta_d0 = 28.9, beta_d = c(0.3, -0.2), eta_d = c(-0.03, -0.01),

alpha_s = 0.6, beta_s0 = 10.2, beta_s = c(0.3), eta_s = c(0.5, 0.02),

sigma_d = 2.0, sigma_s = 3.0, rho_ds = -0.3)

equilibrium_mdl <- simulate_model("equilibrium_model", parameters, seed, verbose)

fiml_optim_est <- estimate(equilibrium_mdl, control = optimization_control)

fiml_gsl_est <- maximize_log_likelihood(

equilibrium_mdl, step = .01, objective_tolerance = .01, gradient_tolerance = .01)

ls_est <- estimate(equilibrium_mdl, method = "2SLS")

Market classes' design

Remaining models' estimation benchmarks

Equilibrium model

Directional model

Deterministic adjustment model

Stochastic adjustment model

Example

Houses data

data(houses)

| DATE | The date of the record. | |

| HS | Private non-farm housing starts in thousands of units (not seasonally adjusted). | Economic Report of the President (1947) |

| RM | FHA Mortgage Rate series on new homes in units of 100 (beginning-of-month Data). | Fair (1971) |

| DSLA | Savings capital (deposits) of savings and loan associations in millions of dollars. | Federal Reserve Bulletin (1914) |

| DMSB | Deposits of mutual savings banks in millions of dollars. | Federal Reserve Bulletin (1914) |

| DHLB | Advances of the federal home loan bank to savings and loan associations in million of dollars. | Federal Reserve Bulletin (1914) |

| W | Number of working days in month. | Manually collected |

Houses data

house_data <- fair_houses()

| DATE | The date of the record. | |

| HS | Private non-farm housing starts in thousands of units (not seasonally adjusted). | Economic Report of the President (1947) |

| RM | FHA Mortgage Rate series on new homes in units of 100 (beginning-of-month Data). | Fair (1971) |

| DSLA | Savings capital (deposits) of savings and loan associations in millions of dollars. | Federal Reserve Bulletin (1914) |

| DMSB | Deposits of mutual savings banks in millions of dollars. | Federal Reserve Bulletin (1914) |

| DHLB | Advances of the federal home loan bank to savings and loan associations in million of dollars. | Federal Reserve Bulletin (1914) |

| W | Number of working days in month. | Manually collected |

| ID | Dummy entity id | |

| DSF | \(DSLA_{t} + DMSB_t - (DSLA_{t-1} + DMSB_{t-1})\) | |

| DHF | \(DHLB_{t} - DHLB_{t-1}\) | |

| MONTH | Month of the date | |

| L2RM | \(RM_{t-2}\) | |

| L1RM | \(RM_{t-1}\) | |

| L1HS | \(HS_{t-1}\) | |

| CSHS | \(\sum_{s=1}^{t-1} HS_{s}\) | |

| MA6DSF | Moving average of order six of DSF | |

| MA3DHF | Moving average of order 3 of DHF |

Post estimation options

- Demanded, supplied quantities, and aggregation

- Analysis of shortages

- Marginal effects

Demanded, supplied quantities, and aggregation

demanded_quantities(model, est@coef)

supplied_quantities(model, est@coef)

aggregate_demand(model, est@coef)

aggregate_supply(model, est@coef)

Analysis of shortages

shortages(model, est@coef)

shortage_indicators(model, est@coef)

shortage_standard_deviation(model, est@coef)

normalized_shortages(model, est@coef)

relative_shortages(model, est@coef)

shortage_probabilities(model, est@coef)

Marginal effects

summary(model)

Stochastic Adjustment Model for Markets in Disequilibrium

Demand Equation : D_HS ~ D_RM + D_W + D_TREND + D_CSHS + D_MONTH

Supply Equation : S_HS ~ S_RM + S_W + S_TREND + S_MA6DSF + S_MA3DHF + S_MONTH

Price Equation : RM_DIFF ~ (D_HS - S_HS) + TREND + L2RM + L3RM

Shocks : Independent

Nobs : 128

Sample Separation : Not Separated

Quantity Var : HS

Price Var : RM

Key Var(s) : ID, TREND

Time Var : TREND

shortage_probability_marginal(model, est@coef, "RM")

shortage_probability_marginal(model, est@coef, "CSHS", aggregate = "at_the_mean")

shortage_marginal(model, est@coef, "MA3DHF")

More on functionality

Initialization

model <- new(

"diseq_stochastic_adjustment",

c("ID", "TREND"), "TREND", "HS", "RM",

"RM + TREND + W + CSHS + MONTH",

"RM + TREND + W + MA6DSF + MA3DHF + MONTH",

"TREND + L2RM + L3RM + L4RM",

fair_houses() %>% dplyr::mutate(

HS = log(HS),

L1HS = dplyr::lag(HS),

CSHS = cumsum(ifelse(is.na(L1HS), 0, L1HS)),

L3RM = dplyr::lag(RM, 3), L4RM = dplyr::lag(RM, 4)),

correlated_shocks = FALSE)

summary(model)

Stochastic Adjustment Model for Markets in Disequilibrium

Demand Equation : D_HS ~ D_RM + D_W + D_TREND + D_CSHS + D_MONTH

Supply Equation : S_HS ~ S_RM + S_W + S_TREND + S_MA6DSF + S_MA3DHF + S_MONTH

Price Equation : RM_DIFF ~ (D_HS - S_HS) + TREND + L2RM + L3RM

Shocks : Independent

Nobs : 128

Sample Separation : Not Separated

Quantity Var : HS

Price Var : RM

Key Var(s) : ID, TREND

Time Var : TREND

Estimation options

- Keyword options:

gradient %in% c("numerical", "calculated") # default: "calculated"

hessian %in% c("numerical", "calculated", "skip") # default: if not "calculated" then "numerical"

standard_errors %in% c("homoscedastic", "heteroscedastic") ||

standard_errors %in% names(object_to_be_estimated@model_tibble) # default: "homoscedastic"

- Example:

est <- estimate(model, control = list(maxit = 1e+5, reltol = 1e-4),

standard_errors = c("W"))